The AI Compute War: Why Chips, Data Centers, and Power Are Becoming the New Oil

For most people watching the AI race, the story still looks like a model competition. OpenAI releases a smarter model. Google answers with Gemini. Anthropic pushes Claude forward. xAI, Meta, Mistral, DeepSeek, Alibaba, and others try to close the gap. The headlines make it sound like the future belongs to whoever has the best benchmark score, the slickest chatbot, or the most impressive demo video.

That is only the visible layer. Underneath the model race is a much harder, more expensive, and more strategic battle: the race for compute. The real AI war is increasingly about who can secure the chips, electricity, data centers, cooling systems, networking infrastructure, cloud contracts, and capital required to train and run frontier AI at scale. The uploaded newsletter batch pointed to this repeatedly, especially through stories about Google and Blackstone’s TPU cloud venture, Nvidia H200 export politics, power-price pressure from AI data centers, and the broader move toward industrial-scale AI infrastructure.

This is where the AI story gets more serious. A model is not just an algorithm floating in cyberspace. It is the visible output of a gigantic physical machine. Behind every fast AI answer is a chain of GPUs or TPUs, high-bandwidth memory, advanced packaging, networking switches, substations, cooling loops, power contracts, land deals, chip fabrication, export controls, and billions of dollars in capital expenditure. The “cloud” was always someone else’s computer. In the AI era, that computer is becoming one of the most valuable industrial assets on Earth.

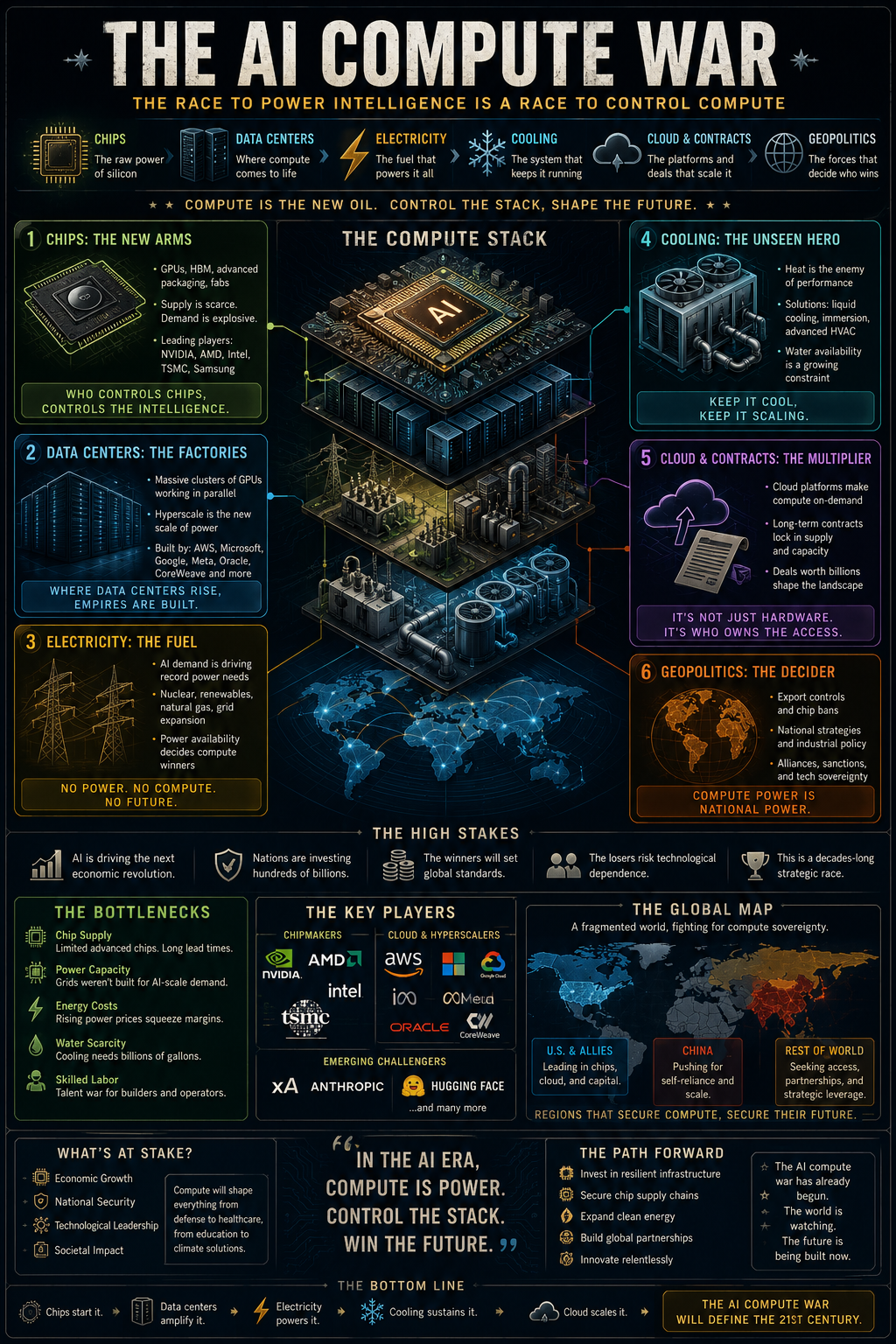

What Is the AI Compute War?

The AI compute war is the competition to control the physical and financial infrastructure that makes advanced AI possible. In simple terms, compute means the processing power used to train and run AI models. In practical terms, it means specialized chips such as Nvidia GPUs, Google TPUs, AMD accelerators, custom AI silicon, networking equipment, storage systems, memory, servers, data centers, and the electricity needed to keep everything operating.

This war has several fronts. The first is chips. Nvidia has dominated the GPU side of the AI boom because its hardware and CUDA software ecosystem became the default platform for training large models. Google has pushed a different path with its Tensor Processing Units, or TPUs, which are custom chips designed for machine learning workloads. Other players are chasing the same prize because AI chips are no longer just components. They are strategic assets.

The second front is data centers. Owning chips is not enough if there is nowhere to put them. Advanced AI clusters need buildings with enormous power capacity, high-speed networking, specialized cooling, security, redundancy, and proximity to reliable energy infrastructure. The third front is electricity. AI is not just computationally hungry; it is power hungry. The International Energy Agency projects that global data center electricity consumption will roughly double from about 485 TWh in 2025 to around 950 TWh by 2030, reaching about 3% of global electricity demand.

The fourth front is geopolitics. Governments increasingly understand that compute capacity affects economic competitiveness, military power, cyber capability, scientific research, and national security. Export controls on advanced chips are not just trade policy. They are attempts to shape who can train the most powerful models and who remains dependent on foreign hardware.

This first image group would work well near the opening section because it gives readers a clear mental model of the compute stack behind AI.

Why People Are Suddenly Talking About Compute

Compute has always mattered in AI, but it used to feel like a technical detail. Researchers talked about model architecture, datasets, training methods, and parameter counts. Hardware mattered, but it was not usually the part of the story casual readers followed closely. That changed when frontier AI became expensive enough that only a small number of companies could afford to compete at the top.

Training a frontier model is no longer like launching a normal software product. It is closer to building a factory. You need land, energy, chips, networking, cooling, staff, financing, and long-term capacity planning. Then, after the model is trained, you still need inference capacity to serve millions or billions of user requests. The cost does not stop when the model launches. In many ways, that is when the cost becomes permanent.

This is why cloud capacity is becoming a competitive weapon. Anthropic announced in April 2026 that it had signed a new agreement with Google and Broadcom for multiple gigawatts of next-generation TPU capacity expected to come online starting in 2027. Anthropic said the deal would support frontier Claude models and help meet customer demand. That is not a casual vendor contract. That is a long-term infrastructure bet.

Google and Blackstone’s new TPU cloud venture pushes the same theme even harder. Blackstone announced a joint venture with Google to create a U.S.-based company offering data center capacity, operations, networking, and Google Cloud TPUs as a compute-as-a-service offering. Blackstone said the new company would give customers another way to access Google TPUs in addition to Google Cloud. Reuters reported that Blackstone would initially contribute $5 billion in equity to develop 500 megawatts of data center capacity by 2027, with the overall investment potentially reaching $25 billion including leveraged financing.

That is the kind of number that reveals the scale of the shift. AI is not being built like a lightweight internet service anymore. It is being financed like heavy infrastructure.

The Google TPU Strategy

Google’s TPU strategy is one of the most interesting parts of the compute war because it challenges Nvidia’s dominance in a different way. Nvidia owns the broad AI accelerator market through GPUs and CUDA, but Google has years of experience building custom silicon for its own workloads. TPUs were originally a way for Google to run machine learning more efficiently inside its own ecosystem. Now they are becoming a product strategy.

The Blackstone partnership suggests Google wants to turn TPU capacity into a broader infrastructure business. Instead of keeping TPUs mostly inside Google Cloud, Google is helping create another channel where customers can access TPU-based compute. That matters because the demand for AI compute is growing faster than traditional cloud capacity can comfortably absorb.

For AI labs, the appeal is straightforward. If everyone is competing for the same Nvidia GPUs, then having access to a large TPU pipeline can become a strategic advantage. For Google, the appeal is also obvious. If more frontier labs and enterprises build on TPUs, Google becomes less dependent on Nvidia’s hardware ecosystem and gains more control over the economics of AI infrastructure.

There is also a deeper strategic layer. Google is not only selling compute; it is connecting compute to models, cloud services, developer tools, and enterprise AI products. Its I/O announcements around Gemini, Antigravity, agentic Search, Workspace AI, and multimodal tools all depend on large-scale compute in the background. The more AI becomes embedded across Google’s product surfaces, the more important it becomes for Google to own as much of the compute stack as possible.

This is why the phrase “AI infrastructure” should not be treated as boring. Infrastructure decides what products are possible, how expensive they are to run, how reliable they feel, and who gets access first.

Nvidia, H200, and the Geopolitical Chip Wall

The Nvidia H200 story shows how quickly AI chips moved from business technology to geopolitical leverage. Reuters reported that the United States approved sales of Nvidia H200 AI chips to around ten Chinese companies, including major firms such as Alibaba, Tencent, ByteDance, and JD.com, but that no shipments had occurred due to complications on both sides.

That is a fascinating situation. On one side, Nvidia wants access to a massive market. On another side, the U.S. government wants to preserve American AI leadership and prevent advanced chips from strengthening rival military or surveillance capabilities. On the Chinese side, companies may want high-performance hardware, but Beijing also wants domestic alternatives and less dependency on foreign technology.

The result is a strange new reality where AI hardware is both a product and a bargaining chip. A chip sale is no longer simply a chip sale. It can involve export licenses, military-use restrictions, revenue-sharing rules, routing requirements, security concerns, and diplomatic calculations. For a technology industry used to globalized supply chains, that is a major shift.

This is why China is pushing so hard on domestic AI chips. If access to frontier compute can be restricted by foreign policy, then dependence on outside suppliers becomes a strategic vulnerability. The same logic applies everywhere. Europe wants more sovereign compute. Middle Eastern countries are investing heavily in AI infrastructure. The U.S. wants to maintain its lead. China wants independence. Cloud providers want locked-in customers. AI labs want guaranteed capacity.

The compute war is not just companies competing for performance. It is countries competing for strategic autonomy.

Power Is Becoming the Hidden Bottleneck

The AI industry can buy chips faster than many regions can build power infrastructure. That may become one of the defining constraints of the next decade. AI data centers need constant, reliable electricity. They cannot simply appear anywhere. They need grid capacity, transmission access, cooling water or alternative cooling designs, backup power, and local political acceptance.

The IEA projects that global electricity generation needed to supply data centers will grow from 460 TWh in 2024 to over 1,000 TWh in 2030 and 1,300 TWh in 2035 in its base case. It expects renewables to meet nearly half of the additional demand over the next five years, followed by natural gas and coal, with nuclear playing a growing role later in the decade.

That forecast matters because AI data centers are not evenly distributed. They cluster in regions with cheap power, available land, strong fiber connectivity, favorable permitting, and proximity to cloud markets. When too many data centers land in the same grid region, they can create local strain even if global electricity demand still looks manageable as a percentage of total consumption.

In the United States, the Department of Energy notes that data center deployment, partly driven by AI, is a significant factor in near-term electricity demand growth. The DOE also cites an Electric Power Research Institute estimate that data centers could grow to consume up to 9% of U.S. electricity by 2030. That is a serious number. Even if the final figure lands lower, the planning challenge is already real.

The public reaction is also changing. People may like AI tools, but they may not want massive data centers raising local electricity prices, consuming water, or changing regional energy planning. This is where the industry’s “AI will transform everything” message runs into local politics. A community may be excited about innovation in theory and still oppose a data center down the road.

Why Data Centers Are the New Strategic Real Estate

In the old internet economy, valuable digital infrastructure meant cloud regions, undersea cables, mobile networks, and hyperscale platforms. Those still matter, but AI has added a new layer of strategic real estate: sites with enough power to host large accelerator clusters. A plot of land with access to hundreds of megawatts of reliable electricity is no longer just industrial real estate. It is AI territory.

This explains why private equity, utilities, cloud companies, and AI labs are suddenly intertwined. Blackstone’s role in the Google TPU venture is a perfect example. Private equity understands long-term infrastructure assets. Google understands AI chips and cloud customers. Together, they are turning compute capacity into an investable infrastructure product.

That model may become common. AI labs need compute but may not want to own every data center. Cloud providers want customers but need capital. Infrastructure investors want long-term cash flows. Utilities want predictable demand but must manage grid reliability. Governments want economic development but also worry about power affordability and national security. These interests are converging around data centers.

For tech enthusiasts, this changes how to read AI news. A model release matters, but so does a power deal. A benchmark matters, but so does a cloud capacity contract. A chip architecture matters, but so does high-bandwidth memory supply. The companies that win AI may not simply be the ones with the cleverest researchers. They may be the ones with the best infrastructure strategy.

The New AI Cost Curve

A major misunderstanding in AI is the assumption that software always gets cheaper in a smooth, predictable way. Historically, digital products often benefited from near-zero marginal cost. Once software was built, adding another user was relatively cheap. AI breaks that pattern. Every serious model interaction consumes compute. Every image generation, video generation, long-context coding session, voice conversation, or agentic workflow creates real infrastructure cost.

That does not mean AI will remain expensive forever. Hardware improves. Models become more efficient. Quantization, distillation, caching, routing, sparsity, smaller specialized models, and on-device inference can all reduce costs. But demand is expanding at the same time. Users do not just want one answer anymore. They want agents that run for hours, generate media, inspect codebases, analyze files, query tools, and act across workflows.

This creates a moving target. Efficiency improves, but workloads become heavier. A chatbot answer is cheap compared with a multimodal agent that reads a repository, runs tests, edits files, generates screenshots, and loops through revisions. A text summary is cheap compared with a high-resolution video model or real-time voice assistant with long session memory.

That is why compute planning is becoming central to AI business models. Companies need to know not only whether users like the product, but whether the product can be served profitably at scale. A viral AI feature can become a financial problem if every user interaction costs too much. The winning companies will be the ones that combine powerful models with smart routing, caching, efficient inference, and disciplined product design.

Evidence Supporters Cite

Supporters of the compute buildout argue that every major technology platform required infrastructure before it became ordinary. Railroads needed tracks. Electricity needed grids. Cars needed roads and gas stations. The internet needed fiber, servers, routers, and data centers. AI, in this view, is simply reaching its infrastructure phase.

They also argue that demand is real. Enterprises want AI coding tools, customer-service agents, analytics automation, document processing, security tools, creative media systems, and internal copilots. Consumers want AI search, voice assistants, image generation, tutoring, financial advice, health guidance, and productivity tools. If these products become daily-use utilities, then massive compute investment is rational.

The IEA’s projections support the idea that data center electricity demand is becoming a major energy planning issue, not a temporary spike. Its base case has global data center electricity use reaching roughly 945 to 950 TWh by 2030, with AI-focused data centers growing faster than overall data center consumption.

Supporters also point out that compute scarcity itself is evidence of demand. If leading AI labs are signing multi-gigawatt capacity agreements and major investors are financing dedicated AI cloud ventures, that suggests the market expects demand to keep rising. Anthropic’s expanded TPU agreement with Google and Broadcom is one example. Google and Blackstone’s TPU cloud venture is another.

The Skeptical View: What If the Buildout Gets Ahead of Reality?

The skeptical view is not that AI infrastructure is useless. That would be too simplistic. The better skeptical argument is that the industry may overbuild before the revenue model fully proves itself. If hundreds of billions flow into data centers, chips, power contracts, and cloud capacity, the returns must eventually show up somewhere. Productivity gains, subscription revenue, enterprise contracts, advertising, automation savings, or new products need to justify the capital.

There is also a risk of regional backlash. Data centers can create jobs during construction, but they do not always create large numbers of permanent local jobs compared with the amount of power they consume. If residents see higher utility bills, strained grids, water concerns, or land-use conflicts, the politics can turn quickly. AI companies may discover that infrastructure approval is not just a technical problem but a trust problem.

Another skeptical angle is efficiency disruption. If smaller models, better inference systems, edge AI, or algorithmic breakthroughs reduce demand for giant centralized clusters, some infrastructure bets could look excessive. The industry has seen this before in other forms: capacity gets built for one assumption, then architecture changes. AI will likely need huge compute, but the exact shape of that demand is uncertain.

The final concern is concentration. If only a handful of companies can afford the compute required for frontier AI, the market may become even more centralized. That affects startups, researchers, open-source communities, universities, and smaller countries. Compute inequality could become one of the defining divides of the AI era.

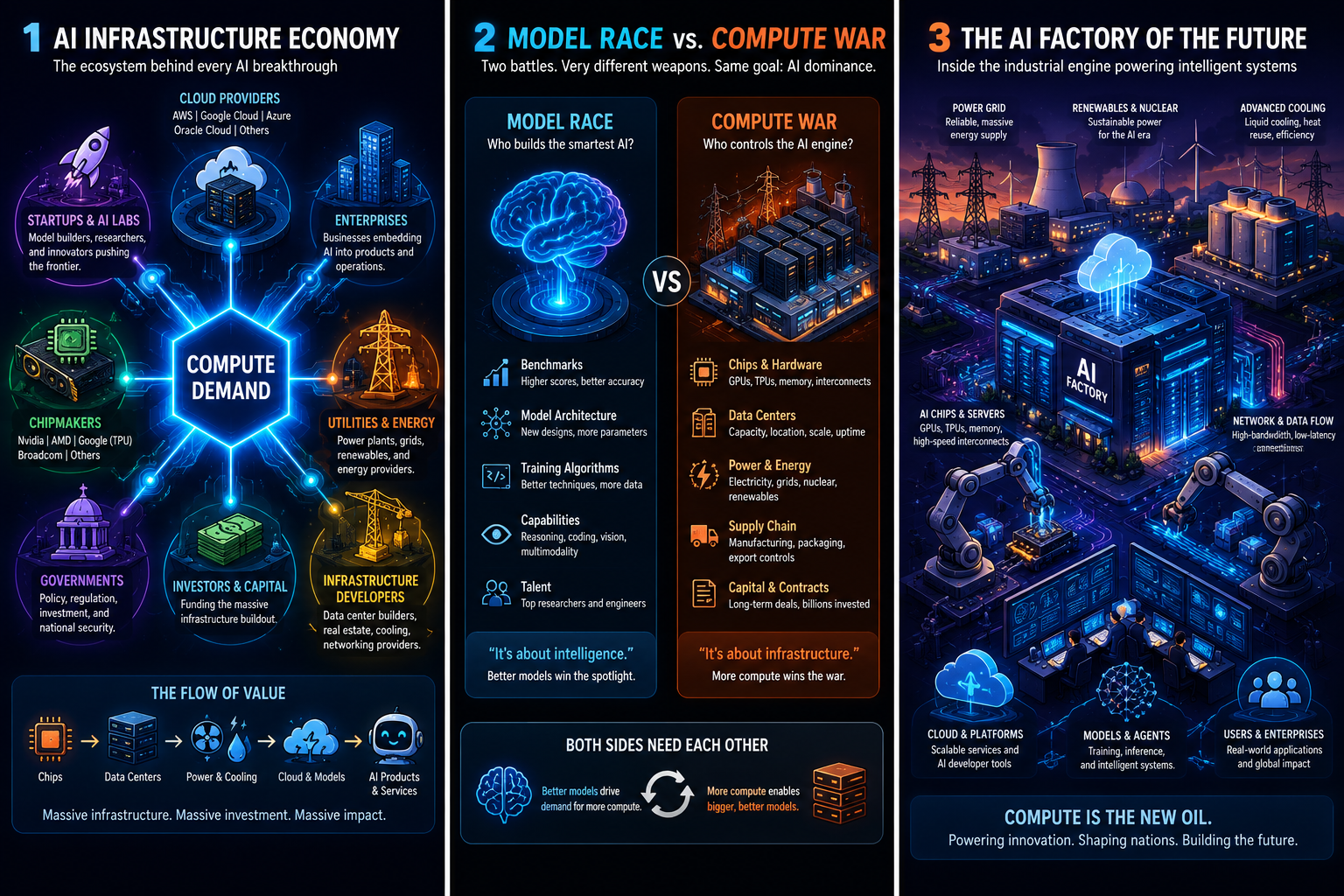

Why This Matters Today

This matters today because the AI race is entering its industrial phase. The first phase was about demos. The second phase was about products. The third phase is about infrastructure. The companies that can secure compute at the right cost, in the right regions, with the right energy strategy, will have room to experiment. The companies that cannot will be forced to ration, rent, or specialize.

For developers and startups, this changes strategy. Not every product should depend on the largest model for every task. Smart builders will use model routing, smaller specialized models, caching, retrieval systems, local inference where possible, and careful workflow design. In a world where compute is expensive, efficiency becomes a competitive advantage.

For investors and business leaders, AI infrastructure becomes a key signal. Watch chip supply. Watch data center capacity. Watch cloud commitments. Watch energy contracts. Watch export controls. Watch which labs secure long-term compute and which ones keep hitting usage limits. These may tell you more about the next phase of AI than a flashy model demo.

For ordinary users, the compute war will show up indirectly. It may affect subscription prices, usage limits, product availability, regional rollout speed, electricity debates, privacy tradeoffs, and which AI products survive. When a company changes pricing or limits long agentic workflows, it may not simply be greed. It may be compute economics surfacing through the product.

This third image group would work well near the “why it matters” and final analysis sections, especially if you want the article to feel like a polished FinkleTech feature.

Real-World Application for Tech Enthusiasts

For tech enthusiasts, the practical lesson is to stop judging AI companies only by model intelligence. Model quality still matters, but infrastructure quality is now part of product quality. A brilliant model that users cannot access reliably is less useful than a slightly weaker model that is fast, cheap, and always available.

This also means learning the AI stack more deeply. The important vocabulary now includes GPUs, TPUs, HBM, inference, training clusters, power usage effectiveness, liquid cooling, interconnects, model routing, caching, quantization, and data center capacity. These are not side topics anymore. They are part of understanding how AI actually works in the real world.

If you are a builder, the smartest approach is not to copy the frontier labs. You probably cannot outspend them. Instead, build around constraints. Use smaller models where they are good enough. Keep prompts lean. Cache repeated work. Avoid unnecessary long-context calls. Design agents that do fewer, better steps instead of looping endlessly. Use human approval where it saves wasted compute. Treat tokens like money because, at scale, they are money.

If you are creating content, this is a great time to educate readers on the physical side of AI. Most people still think AI is just a website. Showing them the chips, grids, power plants, cooling systems, export controls, and financing behind the chatbot makes the story more grounded and more interesting. It also gives your tech site a more serious edge.

Final Verdict: AI Is Becoming an Industrial Power Game

The AI compute war is not a side story. It may be the main story. Models get the attention because they talk, generate, code, and create. But the models are downstream of compute. Whoever controls affordable, scalable, reliable compute controls the pace of frontier AI development.

The next winners in AI will not be decided only by clever prompts or beautiful interfaces. They will be decided by infrastructure: who gets chips, who gets power, who builds data centers fast enough, who secures long-term cloud capacity, who avoids geopolitical chokepoints, and who can turn massive compute spending into profitable products.

The skeptical reader should not ignore the risks. There may be overbuilding. There may be local backlash. There may be energy strain. Some companies may discover that users love AI but not enough to pay what it costs to serve. The industry still has to prove that the infrastructure boom produces durable economic value rather than just impressive demos and giant electricity bills.

But the direction is clear. AI has moved out of the lab and into the power grid. It has moved from software strategy into industrial strategy. The race is no longer just about who has the smartest model. It is about who can build the machine behind the machine.

That is why chips, data centers, and electricity are becoming the new oil of the AI age.

2 Relevant External Links

The International Energy Agency’s Energy and AI analysis is a strong source for understanding how data center electricity demand is expected to grow through 2030.

Blackstone’s official announcement of its joint venture with Google is useful for understanding how TPU cloud infrastructure is becoming a major investment category.